Snap Finance – A Funding Choice for Individuals With Bad Credit

While the initial article provided a good overview of Snap Finance, a monetary innovation organization offering portion credits to those with terrible credit. Figure out how it functions, who can benefit, and the upsides and downsides. Assuming you’re thinking about Snap Finance, read on for significant experiences. In the present speedy world, monetary adaptability is critical. However, consider the possibility that your financial assessment isn’t in the best shape. This is where Snap Finance steps in. In this article, we’ll plunge profound into Snap Finance, revealing insight into what it is, the means by which it works, who can utilize it, and the benefits and hindrances it conveys. In this way, on the off chance that you’re searching for a supporting choice notwithstanding having terrible credit, continue to peruse.

What is Snap Finance?

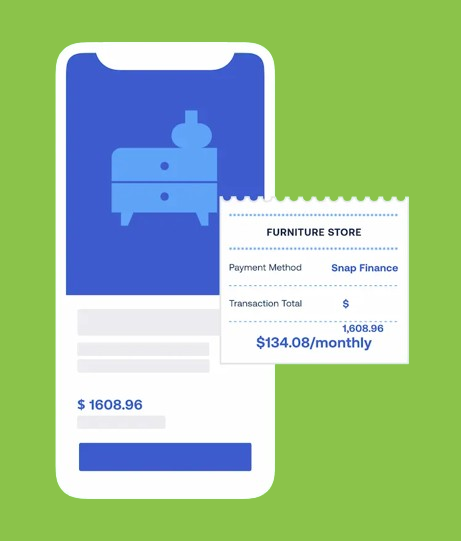

Snap Finance is a monetary innovation organization that has some expertise in furnishing portion credits to people with terrible credit. These advances are commonly utilized to finance critical buys, including furniture, hardware, and domestic devices. Yet, what separates Snap Money?

Snap Finance credits accompany fixed regularly scheduled installments and loan fees, giving consistency in your monetary preparation. This can be especially valuable in the event that you’re attempting to adhere to a financial plan. Furthermore, the approval process for Snap Finance loans is often swift and straightforward.

How does Snap Finance work?

To apply for a Snap Finance loan, you’ll need to supply basic information like your name, address and income. Snap Finance then reviews your credit history and other factors to determine your eligibility. If approved, you’ll receive a lump sum, which you can use to make your desired purchase. Subsequently, you’ll make monthly payments covering both the principal loan amount and interest.

Check More On There Official Website :

Who can use Snap Finance?

One of the standout features of Snap Finance is, it is accessibility to people with bad credit. Nevertheless, specific eligibility requirements must be met:

1. You should be atleast 18 years of age.

2. Possess a valid Social Security number.

3. Demonstrate a steady source of income.

4. Successfully pass a credit check.

Snap Finance’s willingness to work with individuals who have less-than-ideal credit histories is a boon for those looking to rebuild their financial standing.

Benefits of Snap Finance:

1. Access to Essential Goods:

For people with limited financial resources or poor credit, Snap Finance provides a crucial lifeline. It grants access to essential goods like refrigerators, washing machines, furniture, and electronics, potentially improving quality of life. This access can be particularly valuable for families or individuals starting fresh.

2. Building Credit Potential:

Consistently making on-time payments with Snap Finance can positively impact your credit score. This improvement can open doors to other financial opportunities in the future, like lower loan interest rates or more favorable credit card terms.

3. Fixed Monthly Payments:

Unlike traditional loans with variable interest and late fees, Snap Finance’s fixed monthly installments offer predictability and ease of budgeting. You know exactly how much you owe each month, simplifying financial planning.

4. Convenient and Quick Approval:

Compared to traditional lenders with lengthy application processes and stringent credit score requirements, Snap Finance boasts a faster and more accessible application process. This advantage can be appealing for those needing immediate solutions.

5. Transparency and Upfront Fees:

Snap Finance strives for transparency by disclosing all fees upfront. This avoids unpleasant surprises and promotes informed decision-making.

Cons of Snap Finance:

1. High Interest Rates:

Unfortunately, the convenience of Snap Finance comes at a cost. Interest rates tend to be significantly higher than traditional loans, especially for individuals with poor credit. This can lead to paying considerably more for the item over time.

2. Debt Trap Potential:

While manageable monthly payments might seem attractive, the inherent LTO model can lead to a debt trap. You’ll be making payments for longer, potentially hindering your ability to save or invest in other areas.

3. Risk of Losing the Item:

If you miss payments or default on the lease, you risk losing the item and any money already paid. This can be emotionally and financially taxing, so responsible borrowing is crucial.

4. Ownership Implications:

Remember, under LTO, you don’t truly own the item until the final payment is made. Until then, the item belongs to Snap Finance, which may affect insurance options or your ability to move freely with the item.

5. Temptation of Overspending:

The ease of access to financing could lead to impulsive or unnecessary purchases. It’s essential to stick to your budget and only finance items you truly need and can afford to repay.

Beyond the Pros and Cons: Consider These Additional Factors:

1. Compare Alternatives:

Before committing to Snap Finance, explore other financing options like personal loans or credit cards. Evaluate interest rates, terms, and overall costs to find the most favorable solution for your situation.

2. Assess Your Needs and Budget:

Carefully analyze your needs and create a realistic budget. Prioritize only essential items and ensure you can comfortably afford the monthly payments without straining your finances.

3. Read the Fine Print:

Scrutinize the loan agreement thoroughly before signing. Pay close attention to interest rates, fees, default terms, and the total cost of ownership. Do not falter to ask questions if anything is unclear.

4. Practice Responsible Borrowing:

Borrow only what you truly need and can repay responsibly. Prioritize building your credit score through other means to access more favorable financing options in the future.

5. Seek Financial Guidance:

If you’re unsure about your finances or the LTO model, consider seeking professional financial guidance from a trusted advisor. They can help you make an informed decision that aligns with your long-term financial goals.

Snap Finance: A Tool, Not a Solution

Remember, Snap Finance is a tool, not a solution. While it can provide vital access to necessary goods and potentially rebuild credit, overreliance or irresponsible use can lead to financial difficulties. By understanding the pros and cons, comparing alternatives, and practicing responsible borrowing, you can utilize Snap Finance to your advantage and avoid potential pitfalls.

Real-World Insights: Case Studies

For a deeper understanding, let’s explore specific examples of how Snap Finance might be helpful or potentially detrimental in different scenarios:

Case Study 1: Single Mother Needing Essential Appliances:

Mary, a single mother with limited income, desperately needs a new refrigerator for her family. After researching alternatives and confirming affordability, she utilizes Snap Finance to purchase the appliance. By consistently making payments, she improves her credit score and eventually owns the refrigerator outright, significantly enhancing her family’s quality of life. This case exemplifies how Snap Finance can provide access to essentials for those with limited resources.

Case Study 2: Impulsive Furniture Purchase:

Young couple, Jake and Emily, get carried away by the convenience of quick approval and finance a brand-new living room set through Snap Finance. While the monthly payments seem manageable initially, they soon struggle to afford them, neglecting their savings goals and putting a strain on their relationship. This case highlights the potential debt trap of Snap Finance due to impulsive purchases and high interest rates.

Broader Socio-Economic Implications:

Beyond individual benefits and drawbacks, LTO models like Snap Finance raise broader concerns:

Debt and Inequality: Critics argue that LTO models can exacerbate existing debt problems and contribute to wealth inequality. High interest rates can trap individuals in a cycle of debt, particularly those with limited financial resources.

Predatory Practices: Concerns exist about potentially predatory practices within the LTO industry, with some lenders targeting vulnerable demographics with misleading advertisements or unclear terms.

Financial Education: Addressing these concerns necessitates increased financial education and awareness, empowering individuals to make informed decisions about LTO options like Snap Finance.

Evolving Landscape of Financial Services:

As technology and financial services evolve, the LTO model and companies like Snap Finance will likely continue to undergo scrutiny and discussion. It’s essential to stay informed, advocate for responsible lending practices, and empower individuals to make informed choices when navigating the complexities of financing options.

Should I Use Snap Finance?

Whether Snap Finance is the right choice for you depends on your unique circumstances. If you find yourself in need of financing for a substantial purchase and have bad credit, Snap Finance can offer a solution. However, it’s imperative to carefully scrutinize the loan terms. Ensure that you can comfortably manage the monthly payments and are content with the interest rate.

Conclusion:

Snap Finance can be a valuable tool for individuals with limited financial resources or access to traditional loans. However, it’s crucial to be a responsible borrower and weigh the long-term implications carefully. Always prioritize your financial well-being by considering alternatives, assessing your needs realistically, and practicing responsible borrowing habits. Snap Finance can be a stepping stone towards improved financial management, but only when used with awareness and planning.

FAQs about Snap Finance

Q1. What is Snap Finance?

Ans. Snap Finance is a financial technology company offering installment loans to individuals with bad credit, primarily for significant purchases like furniture and electronics.

Q2. How does Snap Finance work?

Ans. To apply, provide basic information, undergo a credit review, and, if approved, receive a lump sum for your purchase. You’ll then make monthly payments, including interest, to repay the loan.

Q3. Who can use Snap Finance?

Ans. Snap Finance loans are available to individuals with bad credit, provided they meet specific requirements, including being at least 18 years old, having a valid Social Security number, and demonstrating a steady income.

Q4. What are the pros of Snap Finance?

Ans. The pros of Snap Finance include accessibility for those with bad credit, fixed monthly payments, and quick approval.

Q5. What are the cons of Snap Finance?

Ans. On the flip side, Snap Finance may have high interest rates, pose difficulties for those with low incomes, and potentially damage your credit score if you default on the loan.

Q6. Should I use Snap Finance?

Ans. Whether you should use Snap Finance depends on your individual circumstances. It can be a suitable option if you need financing for a significant purchase but make sure to review the loan terms to ensure they align with your financial capabilities.

3 thoughts on “Snap Finance”